Gyan Management

Search

Search

Jigna Trivedi1  , Bindiya Soni2 and Priyanka Batra1

, Bindiya Soni2 and Priyanka Batra1

1Shri Jairambhai Patel Institute of Business Management and Computer Applications, National Institute of Cooperative Management (NICM), Gandhinagar, Gujarat, India

2Anand Institute of Management and Information Science, Anand, Gujarat, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-Non Commercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

This study aims to explore the use of storytelling methods as a pedagogical tool to introduce financial literacy concepts to students in Grades 6, 7 and 8. With growing concerns around low levels of financial awareness among schoolchildren, this research attempts to test whether moral-based narratives can be effectively used to teach essential personal finance concepts such as saving, borrowing, investment and ethical earning. The study followed a three-phase structure. In Phase I, a pre-test was conducted to assess students’ existing knowledge. In Phase II, a story was narrated to students using the character of ‘Raju’ to embed core financial lessons through real-life scenarios. Phase III involved a post-test with MCQ-format questions that measured students’ understanding of financial and indigenous knowledge concepts. The study was conducted in an Indian school setting, using purposive sampling and classroom observation. The results revealed a significant improvement in students’ conceptual clarity post-intervention. Most students could now differentiate between needs and wants, understood the importance of saving, and became aware of borrowing risks. Concepts such as income diversification, asset protection, and ethical money habits, which were previously unknown, were now clearly understood. The story format allowed students to engage, reflect, and retain concepts better than formal methods. The study demonstrates that storytelling rooted in Indian cultural values can serve as an effective, low-cost, and engaging pedagogy for imparting financial literacy at the school level. It also highlights the gap in formal curriculum and household financial discussions, making a case for structured interventions through creative means.

Financial literacy, Indian knowledge system, personal finance, school education, storytelling pedagogy

Introduction

In an era where children are gradually exposed to digital transactions, advertisements, and consumer choices from a young age, financial literacy for middle school students has become more essential than ever before (Acar, 2023; Amagir et al., 2018). These formative years represent a crucial stage in the cognitive and behavioural development of children, during which early financial understanding can shape lifelong habits and attitudes (Agasisti et al., 2022; Agnew & Harrison, 2015). However, studies have shown that many children at this level lack even the most basic financial knowledge, such as the value of saving, budgeting, or differentiating between needs and wants (Cortés-Morales & Main, 2022). Hence, the absence of age-appropriate and engaging financial education raises important concerns for educators and parents alike.

Over the past decade, there has been a significant rise in global research on student financial literacy. According to the Scopus database, scholarly publications in this domain have increased fourfold, from 12 papers in 2015 to 48 papers in 2024. This growth reflects three distinct phases: the initial period (2015–2017) with minimal activity, a rapid expansion phase from 2018 to 2021, partly influenced by the financial uncertainties of the COVID-19 pandemic and a more mature phase from 2022 to 2024, where research activity remained consistently high (Irianto et al., 2025). Thus, this trend highlights a growing academic recognition of the need to build financial capability in children and adolescents.

Despite this growing attention, one critical gap persists: the methods used to teach financial literacy to children often remain overly formal, abstract, or disconnected from their everyday realities (Brown et al., 2018; Kaiser & Menkhoff, 2020). Rath and Patra (2023) argue that standard classroom instruction and textbook-based financial lessons may not resonate with younger students, especially in a country like India, where learning is deeply influenced by tradition, culture, and storytelling. Therefore, rethinking pedagogy becomes imperative.

India has a long-standing tradition of using storytelling as a tool for moral and practical education. Classic narratives like the Panchatantra, Jataka tales, and local folklore have for centuries conveyed life lessons in a form that is both engaging and memorable (Rath & Patra, 2023). These stories used simple characters and relatable dilemmas to teach values such as honesty, foresight, and prudence, that align naturally with the core ideas of financial literacy (Amagir et al., 2018; Andriichuk, 2021). But while storytelling remains culturally relevant, it has seldom been explored systematically in the context of financial education for school children.

Therefore, this research attempts to bridge that gap by exploring how ancient Indian storytelling techniques can be effectively adapted to introduce modern personal finance concepts to students in Grades 6–8. The goal is not only to improve financial understanding at an early age but also to make the learning process more meaningful, culturally grounded, and developmentally appropriate. In doing so, the study aims to contribute a pedagogical, moral-based story that integrates traditional narrative methods with contemporary financial education.

Review of Literature

The basic aim of this study is to assess the effectiveness of storytelling as a pedagogical tool in imparting and enhancing students’ understanding of personal finance concepts such as expenses, savings, investment, banking, mutual fund and financial planning among students of Grades 6, 7 and 8 in English medium schools of Anand, Ahmedabad, and Gandhinagar cities in Gujarat. The second objective of the study is to develop a tool from a story that would help to objectively measure the financial literacy of the school kids. The present study tries to teach the financial concepts and core concepts of the Indian Knowledge System (IKS) to the students in a simple and lucid manner.

The theoretical framework of constructivist learning and narrative transportation theories can be used to explain the foundation of the present study. Piaget, Vygotsky and Bruner have majorly contributed to constructivism. They found that learners build knowledge by connecting new concepts to prior experiences and through interactions with their social and cultural environment (Chand, 2024). Further, Bruner’s seminal work (1983) emphasised that education is not a fixed or natural process. Rather, it is designed as a symbol of culture by the communities that can evolve to reflect the shared values. The fundamental theme of the present study, that is, adopting storytelling pedagogy to teach financial concepts, aligns with the principles of constructivism, wherein the learners can acquire this knowledge by relating themselves with familiar and real-life scenarios. Another theory, that is, the Narrative Transportation Theory, by Green and Brock (2000), complements this perspective and explains how people become mentally and emotionally engaged in a narrative. In this psychological condition of transportation, an individual’s attention, imagination and feelings become situated in the narrative, which allows there to be less counter-arguing and more acceptance of the propositions in the story. In addition to this, Green and Appel (2024) thorough chapter advances this concept of narrative transportation by providing examples of how stories can transform individuals and impact beliefs, emotions, identity and social cognition. The narrative transportation theory may be highly relevant to the present study, particularly in imparting financial education. The attention and the engagement levels of the learners expand when budgeting, interest compounding, saving, investing or risk diversification are explained with interesting stories. This increased transportation may improve their understanding, retention, and confidence. Stories that show characters dealing with real-life financial challenges, such as managing debt or saving for a goal, help learners visualise the consequences. They can relate to the characters of the story and understand the financial lessons more effectively than through traditional instruction. Hence, narrative transportation offers a strong theoretical basis and a way to assess how well storytelling works as a teaching method in financial literacy education. Thus, constructivism details how learners actively build contextualised knowledge, while narrative transportation explains why stories are effective in attracting attention and encouraging enduring persuasion. The combination of these principles is also useful for devising meaningful and engaging storytelling interventions.

An individual can make an informed choice of investing their financial resources if they have the essential financial literacy skills. Further, if these skills are taught at a younger age, they can contribute to the long-term financial well-being of an individual. Many empirical studies have analysed the evolution of financial education programmes, especially through storytelling pedagogy from the basic level to the advanced transmedia applications. According to the Discussion Paper Series on financial literacy education by Compen et al. (2019), most of the present knowledge and practice remain rooted in a functionalist paradigm that privileges the transmission of technical knowledge and skills over holistic or critical modes. While the conventional models can produce short-term coding of knowledge, they are typically poor at developing deeper engagement, contextual understanding, or long-term behavioural change. Extant literature on financial literacy education programmes noted that various experiential learning interventions, such as simulations, project-based assignments or assignments pertaining to real-life scenarios, tend to increase the financial knowledge of the students studying in the schools (Batty et al., 2015). This finding was validated in the systematic literature review conducted by Amagir et al. (2018) on financial literacy education programmes for children and adolescents. The authors also reported that the actual behavioural change was found to be limited, though these interventions produced a promising impact in fostering meaningful engagement and behavioural intentions. The pedagogy adopted by the present study, that is, storytelling, cannot be classified as a component of experiential learning but shares the same objective, that is, fostering engagement and contextualising the relevance. This pedagogy, based on narratives, leverages the power of stories rather than hands-on tasks in the experiential learning method. Thus, this study aims to explore an alternative pathway to achieve the same underlying objective of deepening financial literacy. There are studies in the literature confirming the effectiveness of storytelling pedagogy to teach financial concepts to students at the primary school level. Kuswati (2019) and Utie et al. (2025) reported the importance of adopting narratives in enhancing the understanding of financial concepts at an early age among elementary school students. Building upon these foundational studies, the research in the domain of financial education has progressed to developing structured educational materials addressing the needs and preferences of adolescents. Irianto et al. (2024) used the Fuzzy Delphi method to conduct need analysis for the development of storybooks relating to financial literacy for junior high school students.

Blue and Grootenboer (2019) suggested moving away from a conventional approach to teach financial literacy and adopting a praxis approach that integrates moral, ethical and caring dimensions of teaching. The authors strongly recommended that educators recognise how socioeconomic and cultural factors shape the financial choices of an individual. In a way, storytelling pedagogy adopted in the present study can be viewed as complementary to the praxis approach and can serve as a foundation on which more critical praxis-oriented financial literacy can be built.

Very recently, researchers have explored the transmedia storytelling approach involving delivering the content across multimedia to create an engaging experience for the learners. Researchers have applied this novel approach in the landscape of financial education (Santos et al., 2025). Through a pilot evaluation, Freitas et al. (2025) found that this approach of storytelling increased the knowledge and engagement of young adults in financial education. A study testing the efficacy of four novel education programmes with visual interactive tools and digital narratives by Lusardi et al. (2017) also concluded that, with these tools and narratives, the financial literacy scores and the level of confidence of the participants increased significantly. Findings of Fan and Chen (2023) supported this approach and proved that integration of content and language learning with digital storytelling has shown promise in enhancing financial literacy. Further, the systematic literature review by Amagir et al. (2018) reported that knowledge tests, which were able to capture the short-term gains in financial knowledge, have been mostly used by the interventions, and the present study also aligns with the class test approach to assess the learning outcomes of financial literacy taught through storytelling.

The progression from traditional storytelling methods to advanced transmedia and digital storytelling approaches reflects the dynamic nature of educational strategies in financial literacy, and the present study expands the scope of the extant literature by adopting RBI-designed story as the foundation and further expanding it to teach the lessons related to entrepreneurship, ethics and income diversification.

Methodology

The present research was conducted in three phases, catering to a consolidated sample size of 829 students. The study is based on action research using an intervention-based approach. A structured storytelling session served as a pedagogical tool under this action research. Under the action research method, the modus operandi to conduct the research was modified in all three phases. This research was an experiential journey, accompanied by nostalgic memories. A descriptive research design has been adopted, and data were collected at a single point in time from the respondent.

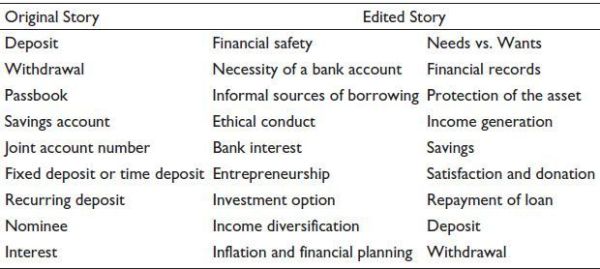

The original story titled, Raju and the Money Tree, in the comic book, written by Manoj and Shailaja in the year 2007, for Issue-I, Basic Banking under RBI Financial Education Series, copyrighted by RBI, was moulded as well as extended to include the other key financial concepts. Considering the short retention span of the students, the story was moulded in such a way that the ideal time to narrate the story was not more than 20 minutes.

The four concepts highlighted in italic were common in the original story and the edited story. As per Table 1, the four concepts highlighted in italic were common in the original story and the edited story. The language used for developing this story was simple and lucid, and it was culturally contextualised to enhance the understanding of the school children. The bilingual mode, that is, English and Hindi, was used to narrate the story.

Table 1. Comparison of Financial Concepts.

The study was conducted in three phases. The first two phases focused on pilot testing and iterative development of the research instrument, while in the third phase, the final data collection was completed with the refined questionnaire. The target audience for all three phases of the study was students from Grades 6, 7 and 8 studying in English medium in either the Gujarat Board or Central Board in Anand and Gandhinagar districts of Gujarat. As the researcher addressed the cohort group, a liberty was taken to address the students of different boards of education. The study settings were the seminar halls of the selected schools in which the students of classes 6, 7 and 8 were addressed simultaneously. To ensure discipline and focused attention, the fellow researchers, student volunteers, and a couple of teachers at the school assisted the researchers till the entire story was narrated, and the questionnaires were filled out by the students.

The instructional phase can be divided into three broad areas, namely, briefing phase, storytelling phase, and debriefing phase. The students were briefed to establish the context. In the briefing phase, the objective of storytelling for teaching financial concepts was revealed. In this phase, it was ensured that interest and excitement were aroused in the students, so that they were deeply engaged when the story was told to them. In the storytelling phase, the researcher orally quoted the entire story from memory, and simultaneously, with the aid of the multimedia projector, the PowerPoint slides were shown, which picturised the entire story. When one researcher was narrating the story, another researcher pointed to the pictures on the PowerPoint slides. In-between the story, the narrator asked questions pertaining to the story, which ensured that students understood what was being told. The narrator tried to encourage students to empathise with the characters of the story and try to predict the outcome by applying financial logic. In the last phase, that is, debriefing phase, a structured debriefing was executed, in which the narrator, for at least 10 minutes, discussed the morals of the story through the reflective questioning method. The morals were the financial concepts that researchers tried to teach.

In Phase I of the pilot testing, 120 students from the selected grades belonging to Anand English Medium School, Anand, were approached for the storytelling session with necessary permissions from the school authorities. Initially, a questionnaire containing 23 items using a five-point Likert scale (5 = Strongly Agree to 1 = Strongly Disagree) was developed to measure the students’ attitude and values aligned with the morals of the story. Initially, it was thought to compare the pre-session and post-session attitudes of the respondents with this questionnaire. However, while conducting the pilot study in Phase I, it was observed that the middle school students were struggling to respond to the statements due to the abstract nature of the scale selected. Some were not able to differentiate among the response options even after explaining to them the statements as well as the scale options in English and Gujarati. Hence, a revision was made, and an emotion-based smiley scale was used for conducting the further study, to make the questionnaire visually appealing and engage the respondents better while responding. Further, minimal variations were observed in the pre- and post-responses. Some statements appeared intuitive enough that the students could answer them without the influence of the story. These observations led to a shift in the approach in Phase II of the pilot testing, which was conducted in Gandhinagar district, where only post-intervention responses were gathered using a smiley-based Likert scale. In the first round, it was also observed that the students were tired of filling out the pre and post-test, so to reduce the fatigue level, the pre-test was strictly omitted. In the second phase, the storytelling intervention was conducted with 388 students of Grades 6, 7 and 8 from Anand Niketan School in Ahmedabad. This second phase revealed that some students experienced response fatigue and struggled with the complex structure of the statements, even when the statements were explained to them in English as well as the Gujarati language by the researchers. Based on these observations, the instrument was further refined. Without compromising on the content, the statements were reduced from 23 items to 16 items. The language part was also simplified to suit the comprehension level of younger students. During this phase, it was observed that the students were not comfortable understanding the expression of the smiley scale. For instance, some students interpreted ‘neutral’ expressions as positive and others as negative. This led to inconsistency in responses and reduced the reliability of the data. Given these limitations, the researchers decided to evaluate the conceptual clarity of the selected students about personal finance concepts through multiple-choice questions (MCQs). Moreover, students were familiar with the concept of MCQs because the teachers often conduct a subject-specific objective test based on the MCQs model. MCQs help to measure what the students have actually learned from the story and are easier to check, score and understand as each question has one clear answer.

Hence, in the final phase, that is, data was collected from 321 students from Mount Carmel High School in the controlled classroom setting, and responses were gathered immediately after the storytelling session to ensure the relevance and recall. The core dataset collected in this phase was analysed with the help of SPSS 21, and scores were calculated for the MCQ to check their knowledge clarity. There were 16 themes or morals identified from the story, on which the questionnaire was framed. The type of questions was either a closed-ended question (8 questions) or a fill-in-the-blanks pattern (8 questions), for which the answer was to be selected from the given four alternatives. In the fill-in-the-blanks pattern question, two questions contained two blanks, so the answer to the question had a joint alternative. The collected data was processed to compute the score. If the student gave a correct answer to the question, then they scored 1 mark, and if the answer was incorrect, then a 0 was assigned. In case of two blanks, 1 mark was assigned only if both the answers were correct. Thus, the MCQ-based questionnaire was 16 marks. In addition to the quantitative analysis, qualitative observations regarding the students’ engagement, understanding, and response patterns were recorded during and after the session to complement the quantitative findings. The data in the respective phases were analysed with absolute numbers, percentages, mean, median, minimum, and maximum. Inferential statistics such as the independent sample t-test and One-Way Analysis of variance (ANOVA) were applied.

The main limitation of this study was the cross-sectional methodology, instead of a longitudinal study, in which the same set of students could have been targeted in all three phases of research. Researchers in future could analyse the sustained knowledge or behaviour change through a longitudinal study. There is also a geographic limitation, because in all three phases, the study was conducted in different schools located in different cities. The board of examination in which the students studied were also different, which might affect the outcome of the study, because there is a difference in the curriculum across each board. A large sample size and wider geographical coverage would provide a holistic picture.

Further, the findings of the study must be applied with caution as the researchers did not consider the control group in the storytelling intervention. The study is subject to post-test bias. The responses of the students after storytelling could reflect their short-term recall ability. There is a possibility that the students would have given socially desirable responses as they know that they are being observed.

Data Analysis

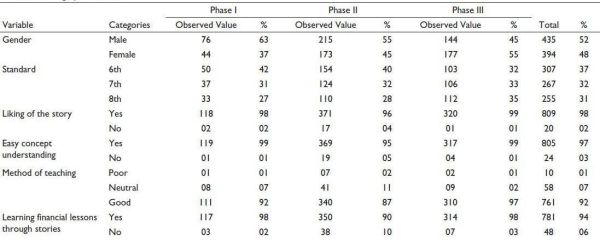

The researcher tried to ask basic information to the students, which is described in Table 2.

From Table 2, it may be inferred that as high as 52% of the respondents were male. A total of 37% of students studied in Grade 6. Nearly 98% of the students liked the story, and 97% of the respondents easily understood the concepts. About 92% of the respondents appreciated the ‘storytelling’ as a useful pedagogy. Furthermore, 94% of the respondents, in future, were enthusiastic to learn the financial concepts through stories.

Table 2. Demographic Details.

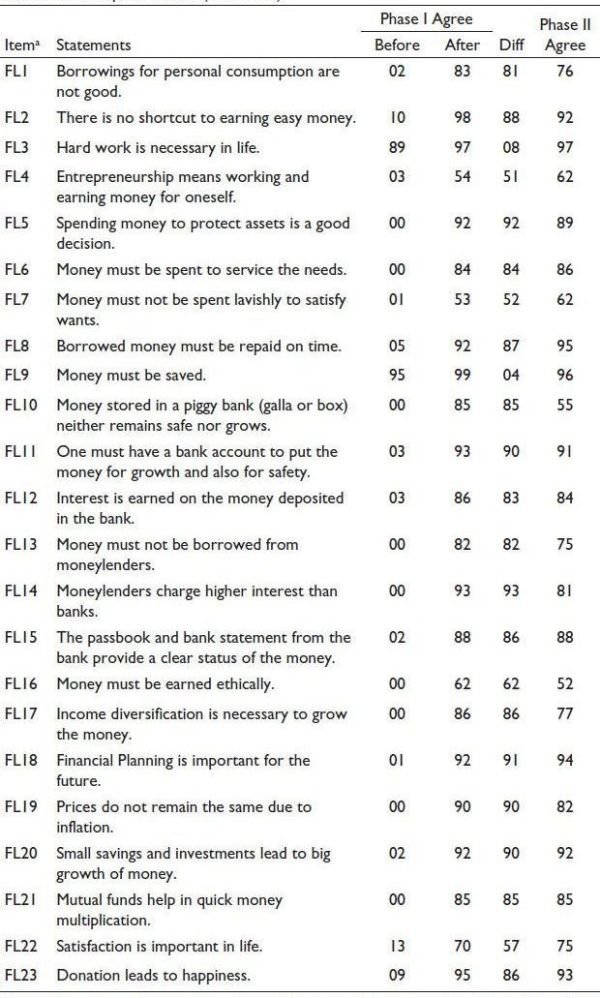

In Phase I and Phase II, it was observed that students could hardly differentiate the 5-point Likert scale without smiley, and the 5-point Likert scale with smiley, so for the analysis purpose, the percentage of before and after, on the anchor point ‘strongly agree and agree were merged as agree’ for the outcome purpose.

It may be inferred from Table 3 that some of the morals of the story were known to the respondents, even before listening to it. The classroom discussion and the informal conversations with the family members, friends, and relatives might have helped them to develop a basic understanding of a few of the financial literacy outcomes. While the students might have learned some basic and core financial concepts from the story.

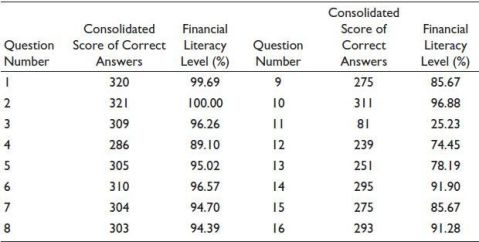

It may be inferred from Table 4 that all 16 questions developed from the story were well-received by the students. Out of the total sample size of 321, more than 230 responses were correct for all questions, except question number 11.

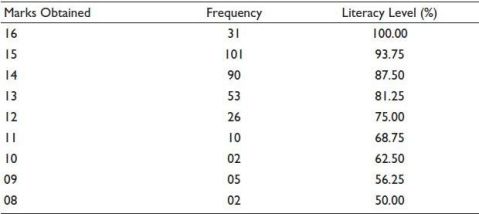

It may be inferred from Table 5 that out of 321 students, only 31 students could answer all questions correctly and scored a full 16 marks. 101 students could correctly answer 15 questions. Ninety students could correctly answer 14 questions. Only two students had a low score of 8.

Table 3. Descriptive Results (in Percent).

Note: aThe items are the outcomes of financial literacy, and they are numbered from FL1 to FL23.

Table 4. Question-Wise Analysis.

Table 5. Overall Score Analysis.

Discussion of the Results

The pen-picture of the main character in the story was a boy named Raju, who was a lazy, non-working fellow. He left his home in search of a money tree and met a fatherly figure, Gopi Chacha, who advised Raju to sow the magical seeds, nurture the plant, and wait for the money to grow on the tree. His intelligent advice transformed Raju into a responsible son, a money-making entrepreneur, and a financially prudent individual. Raju understood the reality of life that money could be generated from undertaking economic activity, and not from myths such as the money tree. Raju’s mother was a torchbearer for his son, who unconditionally cared for him and taught him to adopt ethical means to earn money. The bank manager in the story played the role of an adviser to guide Raju for systematic investment.

From Table 3, it may be observed that in Phase I, the results after storytelling were significantly different. Students understood that borrowings for personal consumption were not good (FL1) and there was no shortcut to earn easy money (FL2), which they might have learned by observing the behaviour of family members (Hang & Thi, 2022; Johnson & Sherraden, 2007). The importance of hard work (FL3) and saving money (FL9) were common cross-table discussions in the Indian middle-class families; there was no significant difference in the scores for the statements, before and after the storytelling (Hang & Thi, 2022). Through the story, the students understood that entrepreneurship meant working and earning money for oneself (FL4). This finding aligned with the findings of Sabau (2022). In reference to the statements FL5, FL6, FL10, FL13, FL14, FL16, FL17, FL19, and FL21, it was observed that students knew nothing before this intervention. Their awareness was very low (score less than 10) with respect to statements such as FL7, FL8, FL11, FL12, FL15, FL18, FL20, FL22 and FL23. However, it may be appreciated that this story was impactful (high score more than 60) in raising the awareness level of the selected school students with respect to the financial literacy outcomes. These findings coincide with the studies of Hang and Thi (2022), Johnson and Sherraden (2007) and Sabau (2022). Thus, it may be inferred that neither informal systems, such as families, friends, and others, nor the class teacher in the formal education system, introduced all of these financial literacy lessons to these children. It is a hard fact that though the economics and finance concepts, such as opening a bank account, simple and compound interest, inflation and many more were specified in the syllabus, students lacked the practical understanding of the same. In Phase II, all the morals of the story were explained through the story, ensuring that the students were attentive, engaged with the central character of the story, and also retained the concept. Thus, the oral communication, accompanied by illustration, ensured conceptual clarity and unforgettable learning (Sconti, 2022). At large, it may be concluded that stories are an effective pedagogical tool to impart knowledge, and further, they are always liked by everyone (Rath & Patra, 2023).

In Phase III of the research, the questions that were framed were linked with the narratives mentioned in the story. Each question rightly addressed the teaching objective required for imparting knowledge of finance and also IKS. Based on the majority of students’ attempts to correctly answer the question, it may be inferred that the story was engaging, students were attentive, and they could comprehend the financial and IKS literacy (Isbell et al., 2004). Moreover, the tool could be treated as effectively designed, because each question framed on the MCQ pattern attained the learning objective. The tool helped to develop the higher-order thinking skills of the students, and the same could be used by other authors to spread the financial and IKS literacy (Amagir et al., 2018). The designed tool to measure the financial and IKS literacy, post storytelling, is presented in Table 6.

Table 6. MCQs Questionnaire for Financial and IKS Literacy.

Note: The answer marked in the italic font indicates the correct answer.

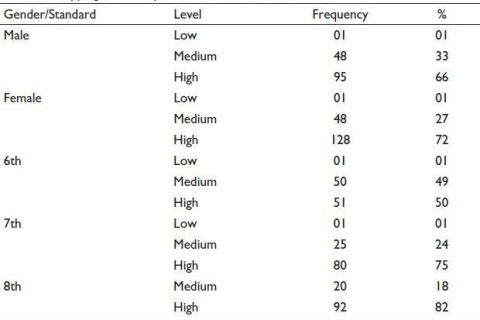

It may be understood that the highest score was 16, with 100% financial literacy level, and the median score of 8 resulted in a literacy level of 50%. The average score across the sample was 15.52 marks. It may be inferred that if the grouping of the literacy level was made on an arbitrary level, then the low literacy score was up to 50%, the medium literacy score ranged between 51% and 82%, and the high literacy score was 83% and above. The financial literacy level was mapped across the gender and the standard of the student.

It may be inferred from Table 7 that female students had higher literacy than male students. It was noted during the qualitative observation that the female students were more attentive during the storytelling phenomenon. An independent sample t-test was run to check the hypothesis, H1: There is no significant difference in the average financial and IKS literacy score between the male and female students. The results from Levene’s test of significance indicated that the assumption of homogeneity of the variance was met, F(1,319) = 1.65, p = .20, thus equal variances were assumed. There was no statistical difference in the literacy scores between males (M = 13.35, SD = 1.61) and females (M = 13.56, SD = 1.50); t(319): –1.22, p = .223. The mean difference (–0.21) was also not significant, and the 95% confidence interval ranged from –0.55 to 0.13.

Table 7. Mapping of Literacy Across Gender and Standard.

Further, one-way ANOVA was conducted to test the hypothesis, H2: There is no significant difference in the financial and IKS literacy score among the students of Grades 6, 7 and 8. Foremost, the assumption of homogeneity of variance was met, as per Levene’s test statistic at F(2,318) = 0.33, p = .719. The statistical difference at the three grade levels, F(2,318) = 4.28, p = .015. On comparison, the descriptive statistics revealed that the mean score for Grade 6 (M = 13.18, SD = 1.55), Grade 7 (M = 13.40, SD = 1.58) and Grade 8 (M = 13.79, SD = 1.47), the score of Grade 8 students was highest. The students of 8th standard who were older in age than the Class 6 and Class 7 students had the highest level of literacy, indicating that the cognitive ability of the child grew with age.

Implications

The outcome of the study offers valuable insights for the educators, policy makers and curriculum designers to strengthen the teaching and learning of personal finance concepts. The improvement in the conceptual clarity of the students studying in Grades 6, 7 and 8 after the intervention of storytelling helped to engage them effectively. They were able to understand and retain the concepts related to finance more effectively as compared to traditional pedagogy. This may serve as a base for the policy makers, such as NCERT, state education boards, RBI, SEBI, and so on, to incorporate the structured modules based on storytelling pedagogy in the curriculum and teacher training programmes can be conducted to assist them in how to handle this intervention. The decision makers can create age-appropriate, story-driven content to promote financial literacy initiatives in the schools. Schools can even collaborate with banks and financial institutions to conduct such story-based workshops to teach concepts such as savings, borrowing, investing, diversification, ethics in earning money, and so on. This pedagogy may be suitable for wider implementation as it does not require many resources. Further, the study offers a simple evaluation framework based on a pre- and post-test model, which can be adapted to monitor the effectiveness of future interventions.

Conclusion

The story-based teaching method helped students grasp important financial concepts in a simple and relatable way. The character of Raju allowed children to connect emotionally, which led to a better understanding of saving, borrowing, and earning. Many students showed improvement in identifying financial terms and applying them to real-life situations.

However, some topics like asset protection, ethical earning, income diversification and long-term financial planning were unfamiliar to most students, indicating the absence of such discussions in both home and classroom environments. The storytelling format made it easier for students to remember lessons, reflect on values, and ask questions without hesitation.

Therefore, storytelling emerged as a meaningful and effective teaching tool, especially for middle school learners. It blended moral learning with financial concepts, promoted curiosity, and encouraged practical thinking. This method is well-suited for the Indian classroom and may be considered as a supplementary pedagogy to strengthen early financial education.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iDs

Jigna Trivedi https://orcid.org/0009-0006-7230-7070

Bindiya Soni https://orcid.org/0009-0002-3640-1386

Priyanka Batra https://orcid.org/0009-0008-1066-1482

Acar, T. O. (2023). Breaking the cycle: The mediating effects of reading, mathematical and literacy skills on financial success in youth. Review of Education, 11(3). https://doi.org/10.1002/rev3.3421

Agasisti, T., Cannistrà, M., Soncin, M., & Marazzina, D. (2022). Financial education during COVID-19: Assessing the effectiveness of an online programme in a high school. Applied Economics, 54(35), 4006–4029. https://doi.org/10.1080/00036846.2021.2016586

Agnew, S., & Harrison, N. (2015). Financial literacy and student attitudes to debt: A cross national study examining the influence of gender on personal finance concepts. Journal of Retailing and Consumer Services, 25, 122–129. https://doi.org/10.1016/j.jretconser.2015.03.006

Amagir, A., Groot, W., Maassen van den Brink, H., & Wilschut, A. (2018). A review of financial-literacy education programs for children and adolescents. Citizenship, Social and Economics Education, 17(1), 56–80. https://doi.org/10.1177/2047173417719555

Andriichuk, V. (2021). Teaching financial literacy in primary school students: International experience. Continuing Professional Education: Theory and Practice, 1, 81–87. https://doi.org/10.28925/1609-8595.2021.1.10

Batty, M., Collins, J. M., & Odders-White, E. (2015). Experimental evidence on the effects of financial education on elementary school students’ knowledge, behavior, and attitudes. Journal of Consumer Affairs, 49(1), 69–96. https://doi.org/10.1111/joca.12058

Blue, L. E., & Grootenboer, P. (2019). A praxis approach to financial literacy education. Journal of Curriculum Studies, 51(5), 755–770. https://doi.org/10.1080/00220272.2019.1650115

Brown, M., Henchoz, C., & Spycher, T. (2018). Culture and financial literacy: Evidence from a within-country language border. Journal of Economic Behavior & Organization, 150, 62–85. https://doi.org/10.1016/j.jebo.2018.03.011

Bruner, J. S. (1983). Education as social invention. Journal of Social Issues, 39(4), 129–141. https://doi.org/10.1111/j.1540-4560.1983.tb00179.x

Chand, S. (2024). Constructivism in education: Exploring the contributions of Piaget, Vygotsky, and Bruner. International Journal of Science and Research (IJSR), 12(7), 274–278. https://doi.org/10.21275/SR23630021800

Compen, B., De Witte, K., & Schelfhout, W. (2019). The role of teacher professional development in financial literacy education: A systematic literature review. Educational Research Review, 26, 16–31. https://doi.org/10.1016/j.edurev.2018.12.001

Cortés-Morales, S., & Main, G. (2022). Needs or wants? Children and parents understanding and negotiating needs and necessities. Childhood Vulnerability, 4, 13–36. https://doi.org/10.1007/s41255-021-00020-5

Fan, T. Y., & Chen, H. L. (2023). Developing cooperative learning in a content and language integrated learning context to enhance elementary school students’ digital storytelling performance, English speaking proficiency, and financial knowledge. Journal of Computer Assisted Learning, 39(4), 1354–1367. https://doi.org/10.1111/jcal.12804

Freitas, C., Santos, A. C., Campos, P. F., Bala, P., & Dionisio, M. (2025). Exploring the impact of transmedia storytelling on financial literacy: A pilot evaluation with young adults. In Proceedings of the 2025 International Conference on Learning Technologies (pp. 853–870). https://doi.org/10.1145/3706599.3719934

Green, M. C., & Appel, M. (2024). Narrative transportation: How stories shape how we see ourselves and the world. Advances in Experimental Social Psychology, 70, 1–82. https://doi.org/10.1016/bs.aesp.2024.03.002

Green, M. C., & Brock, T. C. (2000). The role of transportation in the persuasiveness of public narratives. Journal of Personality and Social Psychology, 79(5), 701–721. https://doi.org/10.1037/0022-3514.79.5.701

Hang, T., & Thi, N. (2022). Financial education in connection to real life for primary school students in Vietnam. International Journal of Education and Social Science Research, 5(2), 208–217. https://doi.org/10.37500/IJESSR.2022.5213

Irianto, O., Susanto, S., Asmaningrum, H. P., & Pasalli, D. A. (2025). Developing financial literacy storybooks for junior high school students: A fuzzy Delphi need analysis. Didaktika: Jurnal Kependidikan, 14(1), 611–620.

Irianto, O., Susanto, S., Asmaningrum, H. P., Rachman, A. M., Budiasto, J., & Sokheh, H. (2024). Storybook validation: Essential practices for students’ financial literacy. Journal of Multidisciplinary Academic and Practice Studies, 2(4), 451–462. https://doi.org/10.35912/jomaps.v2i4.2466

Isbell, R., Sobol, J., Lindauer, L., & Lowrance, A. (2004). The effects of storytelling and story reading on the oral language complexity and story comprehension of young children. Early Childhood Education Journal, 32(3), 157–163. https://doi.org/10.1007/s10643-004-0664-5

Johnson, E., & Sherraden, M. S. (2007). From financial literacy to financial capability among youth. The Journal of Sociology & Social Welfare, 34(3), 119–146. https://doi.org/10.15453/0191-5096.3276

Kaiser, T., & Menkhoff, L. (2020). Financial education in schools: A meta-analysis of experimental studies. Economics of Education Review, 78, 101930. https://doi.org/10.1016/j.econedurev.2019.101930

Kuswati, M. (2019). Development of financial literacy and anti-corruption education in primary schools through storytelling activities. International Journal of Science and Applied Science: Conference Series, 3(1), 75–82. https://doi.org/10.20961/ijsascs.v3i1.32468

Lusardi, A., Mitchell, O. S., & Curto, V. (2017). Visual tools and narratives: New ways to improve financial literacy. Journal of Pension Economics and Finance, 16(2), 1–23. https://doi.org/10.1017/S1474747215000323

Rath, J. P., & Patra, S. (2023). Financial literacy in India: A new way forward. ComFin Research, 11(2), 20–27. https://doi.org/10.34293/commerce.v11i2.6172

Sabau, L. (2022). Digital resources in financial education: Premises for implementation in primary education. Journal of Social Sciences, 5(1), 25–33. https://doi.org/10.52326/jss.utm.2022.5(1).03

Santos, A. C., Campos, P. F., Freitas, C., Bala, P., & Dionisio, M. (2025). A transmedia storytelling experience to engage young adults in financial educational content. In Proceedings of the 2025 International Conference on Learning Technologies (pp. 1–10). Springer. https://doi.org/10.1007/978-3-031-78450-7_3

Sconti, A. (2022). Digital vs. in-person financial education: What works best for Generation Z? Journal of Economic Behavior & Organization, 194, 300–318. https://doi.org/10.1016/j.jebo.2021.12.001

Utie, M. S., Walidain, B., Windiarti, F., Tamimi, Y. A., Lisnawati, R., & Safitri, N. (2025). Peningkatan literasi keuangan sejak dini dengan metode storytelling di sekolah dasar Depok. Jurnal Pengabdian Masyarakat: Pemberdayaan, Inovasi dan Perubahan, 5(1), 1–12. https://doi.org/10.59818/jpm.v5i1.1143