Gyan Management

Search

Search

1University Business School, Panjab University, Chandigarh, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-Non Commercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

Corporate governance has undergone a significant transformation with the advent of digital transformation. However, existing literature on this relationship remains conceptually dispersed and lacks coherence. To address this gap, the present study seeks to assess the interplay between digital transformation and corporate governance by systematically analyzing and summarizing 40 research articles extracted from the Scopus and Web of Science databases. The review follows PRISMA methodology using predefined keywords, inclusion–exclusion criteria, and a transparent multiple screening procedure to provide a systematic and well-organized review of the existing literature. The research findings highlight that digital transformation may enhance decision-making, encourage innovations, and foster sustainability. Nevertheless, it calls attention to a strong regulatory structure to mitigate the associated risk of digital transformation implementation. Additionally, the study reinforces the argument that the corporate governance framework must evolve to account for the transformative impact of digital technologies. The present review extends prior academic understanding of digital transformation and corporate governance and proposes domains for future studies. Further, this comprehensive review offers meaningful insights to boards, policymakers, and regulators on the relationship between digital transformation and facets of corporate governance.

Digital transformation, corporate governance, strategic decision-making, boardroom decision

Introduction

Corporate governance (CG) focuses on enhancing firm’s value through a structured framework and a strong monitoring system (Cuervo, 2002). It is critical to achieve sustainable business growth and stakeholder confidence. CG mechanisms strengthen decision-making, enhance transparency and accountability, and mitigate agency costs (Almubarak & Aljughaiman, 2024). As outlined in the Cadbury Report (1992), CG provides a mechanism for directing and controlling companies. The board of directors (BODs) is responsible for monitoring the governance in companies, while the shareholders hold the authority to appoint directors and auditors, and ensure that an effective governance framework is established. The corporate board is the key CG mechanism. It contributes more expertise and wisdom to the enterprise, enabling uncertainty management and resource accessibility (Hillman et al., 2009). However, the evolution of digital tools has redefined conventional CG practices, entailing funding for financial innovations, reforming governance structures, and reshaping boardroom strategies.

Digitalization replaced the short-term focus of business with long-term sustainable growth. Technology offers a more advanced accountability system for ensuring a transparent, accurate, and real-time flow of information to stakeholders (Varoglu et al., 2021). Investing more in digital transformation (DT) will enhance data storage and make data sharing easier, which will further boost business communication and information. This reduces information asymmetry by dismantling the earlier “information silos” and speeding up internal information flow within the companies (Li et al., 2024). Data-driven insights help boards of directors and CEOs in strategic decision-making. Technology-enabled tools, including artificial intelligence (AI), big data, cloud computing, and blockchain, facilitate continuous monitoring, fraud detection, and compliance management. Yet, technology also brings risks of cybersecurity, moral dilemmas, and legal challenges. Organizations are required to create a strong digital governance structure to maintain a balance between innovation and responsible monitoring.

Digital technologies enable the improvement of CG mechanisms and monitoring practices through strengthening decision-making, implementing IT governance frameworks, and fostering sustainable strategies. Although the research on this relationship has expanded in recent years, the evidence remains fragmented over several theoretical and empirical strands. Hence, a comprehensive review is necessary to embrace diverse insights and broaden knowledge in this emerging discipline. This study seeks to comprehend the understanding of the relationship between DT and corporate governance mechanisms by synthesizing existing evidence and outlining how DT influences key CG dimensions. Accordingly, this study addresses the following research question: How are DT and CG practices interconnected? This systematic literature review adheres to the PRISMA methodology for identifying, screening, and analyzing research articles. The findings will provide valuable insights to researchers, policymakers, and business executives.

Literature Review

The relationship between DT and CG has garnered considerable scholarly attention. Literature reflects how technologically driven improvements disrupt not only business operations but also organizational oversight and compliance systems. Additionally, effective governance mechanisms enable organizations to leverage digital tools for a strategic edge.

Corporate Digital Transformation

DT raised total factor productivity and reinforced governance mechanisms, including internal control and technical cooperation, serving as mediators between DT and productivity. This beneficial effect has been more apparent in non-high-tech corporations, where digitalization significantly strengthens governance and operations, notably when there is diversified executive education and stronger environmental, social, and governance (ESG) performance (Li et al., 2022, 2024).

To optimally leverage DT, firms must establish and evolve dynamic capabilities. Wang et al. (2024) demonstrated that DT augmented green innovation varied across stages, with adaptive and innovative capabilities and leadership commitment fostering outcomes. Yu et al. (2022) revealed that the interaction of strategic focus and operational performance has been mediated by the corporation’s DT capabilities, which include sensing, organizing, and restructuring. DT capabilities have been crucial for innovation and a competitive edge.

Corporate Governance Practices

Resilient governance practices have been playing a crucial role in guiding performance trajectories. Ria (2023) and Danilov (2024) uncovered that CG has been the primary and immediate driver of performance. The independent board, the size of the board, the effectiveness of the audit committee, and higher board activity exerted a substantial and favorable influence on organizational performance and capital structure. However, gender diversity has yielded mixed outcomes. Additionally, Guluma (2021) demonstrated that performance is enhanced by both internal and external CG approaches, such as the degree of product market competition and concentration of ownership.

Danilov (2024) and Guluma (2021) highlighted that profitability has been adversely affected by CG flaws such as CEO duality and overly large boards, underscoring the vitality of well-organized CG mechanisms for facilitating robust monitoring and elevated corporate results.

Broadly, DT and CG have been reinforcing firm-level outcomes.

Interplay of Digital Transformation and Corporate Governance

DT has been redesigning CG through restructuring board roles, competencies, and organizational structure. According to Oliveira et al. (2022), DT has notably influenced board strategic plans, oversight, information-gathering process, and sustainability goals, which have strengthened board capabilities concerning the resource-dependence view. Companies in France, Spain, and Italy have been revamping their governance models by establishing new committees, responsibilities, and reporting practices that have been emphasized on sustainability and digitalization (Capurro et al., 2023).

The successful implementation of DT has required contemporary CG, including a board with high digital proficiency and proactive technological governance. Enterprises with a digitally competent board have realized significantly superior market performance (Ekaterina, 2025).

In aggregate, companies have been adopting digitally focused governance approaches; however, the efficacy of these transformations varies owing to the absence of standardized frameworks and well-defined digital competencies. In parallel, a well-established CG could speed up structured and value-creating DT.

Despite expanding academic interest in DT and CG, the literature on the relationship between DT and CG has remained dispersed, providing scarce insights into how CG facilitates technology adoption or how DT reshapes governance mechanisms. Consequently, there is a need for a comprehensive study that provides an integrated view of the DT–CG relationship.

Methodology

Searching Articles and Selecting Databases

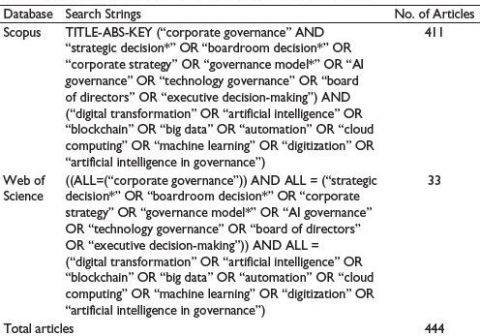

To ensure an extensive overview, the study conducted a systematic literature review. The literature on DT and CG has been found using the Scopus and Web of Science databases. Table 1 represents the search query executed in the databases. This search consists of articles published from 2014 to 2025. The articles available on the databases as of September 16, 2025, were taken into consideration. A 10-year span from 2014 to 2025 was selected to emphasize contemporary research assessing the interplay of DT and CG, taking into account current practices, trends, and empirical insights into their dynamic interrelationship. The initial search yielded a total of 444 articles.

Selecting Criteria

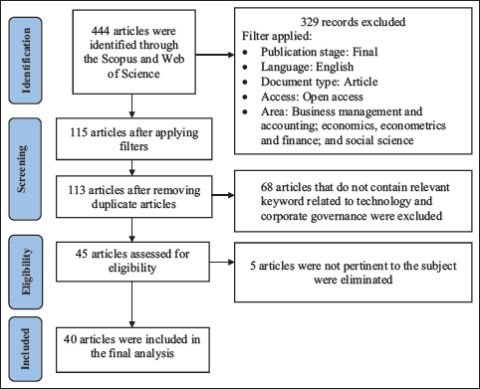

The identified papers were confined to certain inclusion–exclusion criteria to ensure relevance and rigor. First, database filters were applied to include only English-language open-access articles published between 2014 and 2025. Additionally, the articles were limited to Business Management and Accounting; Economics, econometrics, finance, and the social science area for a credible body of evidence, reducing the initial articles to 115. Further, two duplicate articles were removed. Afterward, the title and abstract were screened to select relevant articles in the context of the DT and CG relationship. Finally, full-text reading of articles has been done to retain exclusively those studies that met the inclusion criteria, ensuring robust and insightful analysis. Finally, 40 articles were retained in the sample and systematically classified into themes. Figure 1 represents the selection criteria for the articles.

Table 1. Search Query Employed for Systematic Literature Review.

Figure 1. Phases of Systematic Review.

Findings and Discussions

Journal-wise publications

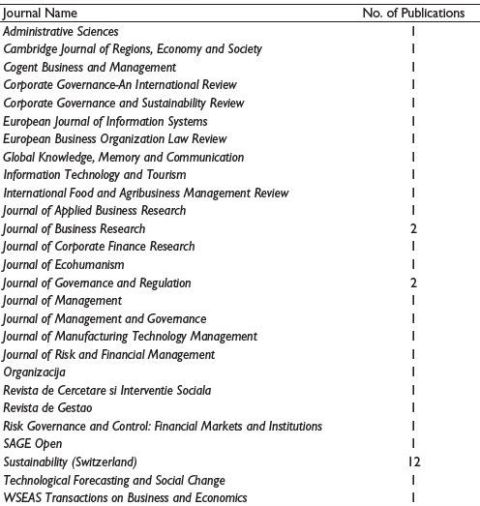

Table 2 represents the distribution of publications across journals, with Sustainability standing out with the highest number, accounting for 12 publications. Following the Journal of Governance and Regulation and the Journal of Business Research, with two publications each. The remaining journals had a count of one. This suggests that research on DT and CG is widely dispersed across different journals. The diversity of journals spanning business, management, finance, technology, and social science indicates an interdisciplinary interest in the subject.

Table 2. Journal-wise Publications.

Year-wise Publications

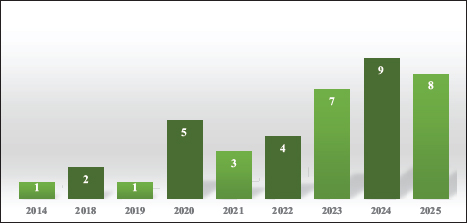

Figure 2 shows the year-wise publications, indicating a significant growth in research output over time, particularly after 2020. The count of publications remained low in the early years, with only one publication in 2014, two publications in 2015, and one publication in 2019. However, there was a sharp rise in 2020 with five publications, followed by some fluctuations in 2021 and 2022. The upward trend continued strongly in 2023 and peaked in 2024 with nine publications, followed by eight publications up to September 2025. The trend suggests growing academic interest in DT and CG.

Thematic Analysis

The study classifies the literature into the following three themes.

Digital-led Governance and Boardroom Decision-making

CG practices have been changing in exceptional ways. The utilization of big data and associated technologies have modified all facets of CG. Businesses could utilize the potent benefits of technology, which has notably improved the quantity and quality of data. This has further impacted efficient resource optimization, minimized operational costs, and raised management efficacy (Lin & Aman, 2025). The London Stock Exchange (LSE) was compelled to demutualize due to heightened competition and technological development. Aligning with agency theory, the LSE has reinforced its financial position after demutualization by reforming its board structure, minimizing the participation of exchange members, and adding more independent directors with varying corporate backgrounds. To support novel strategic objectives, the LSE has restructured its management and implemented pay-for-performance. The results demonstrated that demutualization has upgraded efficiency by integrating with governance and compensation strategies reforms (Angulo et al., 2014).

Figure 2. Year-wise Publications.

Technology-enabled management systems have resulted in intelligent decision-making, management process automation, and real-time data, strengthened core competencies, enlarged market share, and boosted customer trust (Lin & Aman, 2025). Kalkan (2024) examined how AI transforms CG, decision-making, and data transparency. The study demonstrated that AI has enhanced CG by improving decision-making efficacy, risk management, and stakeholder involvement. DT has positively impacted the implementation and efficacy of internal control. Moreover, this association has been more noticeable in corporations with comparatively strong levels of market competition (Wang et al., 2023). Accounting information system (AIS) and non-financial information have been key drivers of effective decision-making and non-financial performance. Additionally, AIS quality contributed to non-financial performance through a sequential mediation pathway involving the combined roles of non-financial information quality and decision-making (Thuy, 2025).

However, literature also disclosed that board members and management have often interpreted and employed big data analytics (BDA) in distinct ways, which could exacerbate information asymmetries and agency problems. BDA use has embodied a dichotomy, whereby managers might exploit it to bias reporting, yet board members could still leverage it for enhanced decision-making (Karamatzanis et al., 2025). Merendino et al. (2018) employed a theoretical lens of the knowledge-based view and cognitive and dynamic capabilities to evaluate the manner and extent by which big data (BD) has affected boardroom decision-making. Findings demonstrated that BODs have confronted a gap in cognitive capabilities to cope with BD and have undergone cognitive biases and overload. Additionally, they have encountered challenges to board cohesion with BD utilization, which may influence decision-making. BD has prompted the BODs to incorporate new working practices beyond conventional boundaries and to leverage third-party capabilities for BD management.

Highly effective BODs have proactively participated in sustainable strategy formation. They have been leveraging their diverse and industry-specific expertise to promote innovation and sustainable value creation (Grove et al., 2021). Diversity in board experience has a notable impact on corporate green technological innovation. The board’s absorptive capacity has amplified this effect. Further, the position of directors within inter-board networks, assessed through network centrality, has enhanced the relationship between board diversity experience and innovation, as well as explicitly influenced innovation (Zhao et al., 2025). In an era of rapid technological advancement, investors in the stock market have given a premium for signals related to the CEO’s commitment to technological innovations. Governance functions have mediated the relationship between the CEO’s inclination toward technology and investors’ assessments of enterprise worth (Filatotchev et al., 2023). Karayalcin (2025) revealed that personal competencies, academic training, and leadership approach have greater influence on innovation than do familial relationships in Turkish family businesses. Family CEOs have exhibited an emphasis on legacy integration and sustainability, while the non-family CEOs have aspired to a long-term strategic approach. However, they have been indistinguishable in their perceived outcome on innovations in products, acknowledging the strategic value of structured innovation processes and risk-seeking propensity. Substantial family engagement has enhanced the favorable impact of family CEO on innovation. Further, female CEOs allocate more resources to innovation. Nevertheless, education has remained crucial for establishing innovation strategies.

The literature revealed that DT has influenced the BODs. The four key facets have been (a) obtaining, analyzing, and disseminating information, (b) board stewardship, (c) strategic planning goals, and (d) blue-sky strategizing (Oliveira et al., 2022). Yan and Yu (2023) investigated how board informal hierarchy influenced digitalization in Chinese corporates from 2012 to 2019, concerning relational contract theory. The study revealed that digitalization and board informal hierarchy have been positively associated. The chairman, in a superior position, has strengthened this relationship. Further, the informal hierarchy has promoted digitalization through enhanced efficacy of BODs’ decisions, reduced managerial myopia, and promoted data sharing. Board size and fintech services have a significant negative relationship, while the independent BODs have enhanced performance through innovation development (Almubarak & Aljughaiman, 2024). Extended board tenure, expanded board networks, and greater gender diversity have enhanced the association between organizational slack and innovation, while larger board size and higher independent BODs have reduced it (Heubeck & Meckl, 2024). Board independence has been favorably related to corporate environmental performance. Utilization of digital technology has a favorable impact on environmental performance in companies with a significant proportion of independent directors. Increased deployment of digital technology alone has not enhanced the corporation’s environmental performance (Napoli, 2023).

Mu et al. (2023) investigated the impact of technology-based firms on performance-based compensation scheme selection from the viewpoint of information asymmetry. The results discovered that performance commitments have been more likely to be achieved with equity, annual, and two-way compensation. Equity compensation and annual incentives have been substantially favorable to accomplishing the target company’s performance obligations. The two-way compensation model has demonstrated a stronger incentive effect on promises. Tech-based corporations should apply equity and annual incentive methods to minimize information asymmetry problems by guaranteeing completion levels. Compensation strategies through enhanced corporate performance have influenced commitment fulfillment. The extent of this influence varied with CG practices and debt payback demands. Additionally, disclosing pay-for-performance has provided a decision-making foundation for commitment agreements.

Figueroa-Domecq et al. (2020) measured the impact of enterprise technology on women’s leadership in the tourism industry and the implications of gender diversity promotion initiatives in the BODs and management teams. The results revealed that an enterprise’s technological level has been positively associated with less involvement of women on the board and in management. Gender diversity initiatives promote women’s representation on the board. Gender diversity requirements on the board have not been minimized, even if AI makes decisions as a board member. Gender quotas have been desired regardless of whether AI has been hired as a director, has been expected to analyze data for decision-making, or has been exclusively utilized to choose directors. Therefore, even though AI would undoubtedly intervene in decision-making, the possibility of biased assessments from AI should not preclude debates about board gender diversity (Eroğlu & Karatepe Kaya, 2022).

IT Governance and Performance Outcomes

Information technology governance (ITG) has become more interdisciplinary, drawing on considerable contributions from other academic specializations such as engineering, computer science, and management. The most credible models reflected crucial theoretical frameworks. ITG research has principally addressed new technologies such as cloud computing and the Internet of Things (Falchi de Magalhães et al., 2021). Tambo and Filtenborg (2019) examined the implications and possibilities of a practically developed ITG framework for the field of technology administration in the IT sector. The study’s findings demonstrated that the ITG framework has offered utility and greater knowledge about the service distribution structure if the value stream approach has been adopted. IT procedures have been more operational and comparable to CG and generic technology management structures.

Chauke and Ngoepe (2024) investigated how multiple ITG aspects have been integrated at the South African Professional Council to establish a framework. The findings revealed that inadequate data management has delayed decision-making, and effective risk management has depended on accountability frameworks. Although organizational knowledge management principles were established, a governance gap resulted from the lack of authorized records management policy. Despite the council following the law’s reporting requirements, insufficient control caused problems with outsourced services. The study proposed that implementing a standardized IT framework has led to data integrity, simplified governance practices, and enhanced organizational efficacy. Lowry et al. (2025) disaggregated ITG into two elements encompassing ITG mechanisms and ITG principles, positing that effective ITG requires embracing principles with strong executive and board-level support. The authors highlighted that the relationship between ITG mechanisms and strategic alignment has been fully explained by Commitment to COBIT Principles (CCP). Moreover, assistance from leadership for IT has reinforced CCP and directly augmented strategic alignment.

ITG has been essential for sustainability and corporate performance, although insufficient knowledge about its structure and contributing factors. The inadequate senior management and IT leaders have created the vulnerability of ITG. The prevailing ITG models have been too basic to consider the industry, size, and maturity variations. This remains valid for SMEs whose ITG adoption and growth have been considerably less, contrasting with large-scale organizations. ITG must be modified to facilitate corporate DT (Levstek et al., 2018).

DT has profoundly impacted governance practices, especially in businesses with dual equity structures, by improving data transparency, effective decision-making, and business oversight. Digitalization has enhanced strategic cost management, streamlined value chains, and provided access to real-time data, which has minimized operating costs and boosted financial performance (Shaohan et al., 2024). Liu and Jung (2024) utilized resource-based view theory to investigate the inherent mechanism of DT on firm performance in Korea and China, with the ESG mechanism playing a mediator. The evidence pointed out that DT has been positively associated with ESG management and firm performance in both countries. Additionally, ESG management and non-financial performance have a positive relationship in Korea and China. However, only Korea showed a positive association between ESG management and financial performance. Further, the ESG mechanism has a positive mediating impact on the association of DT and firm performance.

Capurro et al. (2023) examined the impact of integrated DT into the governance framework on enterprise communication in the Italian, French, and Spanish fashion and food industries. The results have shown favorable integration of new company positions focused on sustainability and digitalization process management. Nonetheless, these responsibilities have diverse effects on CG frameworks and various means of communication with the outside world. Another research reported that online social networking has a considerable governance impact, specifically in non-state-owned enterprises and assisted corporates in minimizing the detrimental impact of investment opportunities and media reporting on investment efficacy. Online social networks, in addition to disseminating information, have connected a broader range of stakeholders. It has successfully made up for media reports’ shortcomings as a CG tool.

AI adoption has played a key role in good governance (Nasr et al., 2024). The adopted AI system has determined its legal accountability for repercussions stemming from its utilization in CG (Yang et al., 2020). The deployment of AI has a substantially favorable impact on the efficacy of CG, reinforcing risk management frameworks and strengthening stakeholder involvement. Through automated monitoring functions, AI has facilitated corporates’ adherence to regulations more efficiently and mitigated human error in reporting. Notwithstanding this, corporates have faced ongoing challenges comprising algorithmic bias, concerns over data privacy, and the requirement for a regulatory framework to align with AI advancements (Shaban & Omoush, 2025). Governance, assurance, and risk management have been pivotal for shaping business strategies and investment decisions. Professionals have been encouraged to leverage emerging technologies, while organizations have been urged to foster innovation and incorporate entrepreneurial orientation in navigating the shift from the fourth to the fifth Industrial Revolution (Nene, 2024).

Risk Management and Sustainability in the Digital Era

DT has enhanced environmental performance by boosting CG practices and green innovation. This outcome has been more apparent in state-owned, large and highly polluted business entities (Xu et al., 2022). Nazzaroi et al. (2022) examined how CG and collective smart innovations contributed to wine cooperatives' environmental and sustainable transformation. The study analyzed the case of La Guardiense. The findings suggested that innovations assisted by governance models have developed economic value. Collective smart innovations have influenced external socially driven economies, including environmental preservation and regional growth, and internal economies such as higher turnover and lower expenses.

The growth of the digital economy has enhanced corporate social responsibility (CSR) activities through boosted online media attention, strengthened agency efficiency, and enabled corporate DT. The local digital economy has influenced varying facets of CSR differently. State-owned firms, secondary industry corporations, large-scale businesses, and non-digital enterprises have encountered greater effects than others (Hu & Liu, 2023).

Ying and Jin (2024) investigated the implications of environmental management system certification (EMSC) and government environmental protection subsidies (EPSs) in market-incentive environmental regulations (ER) on green innovation (GI). Furthermore, the influence of CG and ecological disclosures on the ER–GI relationship of Chinese-listed companies from 2012 to 2021. The findings uncovered that EMSC and EPSs have favorably impacted GI. CG and environmental disclosures have a moderating effect on this relationship. GI has significantly enhanced ESG ratings, and GI combined with ESG has enhanced financial performance. ESG has a mediating impact on fostering GI and economic performance. Further, political affiliation and regional-level innovation have adversely moderated the green innovation-financial performance relationship (Zheng et al., 2022).

However, critical challenges, including algorithmic prejudice, data privacy, and regulatory concerns, need to be addressed (Kalkan, 2024). Grove et al. (2020) explored the key threats, challenges, and opportunities of AI in governance mechanisms. AI has been improving governance practices; however, significant threats include substituting AI for human activities, effective AI management, controlling human–AI relationships, and challenging digital dashboards and quantum computing.

The literature has highlighted critical threats that have impacted CG, including deep shift risk, global economic uncertainties, digital risk, data security risk, diversified consumer expectations, and reputational risk. CG has to comprehend and control these technical threats to strengthen the governance framework and successfully retain competitive advantage. Further, boards of directors need to take proactive measures to deal with technological change to gain investor trust. It has been essential to minimize interruptions from AI or variations in employee behavior for long-term success (Grove et al., 2020).

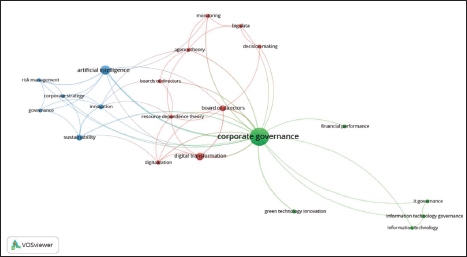

Keyword Analysis

Figure 3 represents the co-occurrence network that demonstrates three clusters created from the keywords defined by the authors. The red cluster of co-occurring keywords reflects emerging research domains encompassing DT, BODs, decision-making, and monitoring. Also, agency theory and resource dependency theory appear as keywords in this cluster. The green cluster highlights key areas explored in recent studies, including information technology, IT governance and financial performance, accounting for integration of IT governance and performance outcomes. The blue cluster, composed of AI, innovation, risk management, and sustainability keywords, reveals prominent trends in the literature.

Figure 3. Co-occurrence Network of Author-defined Keywords.

Source: Authors’ representation using VOSviewer.

Findings

The reviewed articles are analyzed and outlined thematically in this section, underscoring the interplay between DT and CG.

As documented by the analyzed scholarly literature, DT is a strategic asset for streamlining processes and curtailing spending. It further equips managers with efficient decision-making (Kalkan, 2024; Lin & Aman, 2025). However, this is particularly noteworthy in markets characterized by intense competition (Kalkan, 2024). Digital tools such as AIS and BD upgrade decision quality (Karamatzanis et al., 2025; Thuy, 2025). Nonetheless, optimal deployment is occasionally obstructed by board cohesiveness and limited board capabilities, aligning with the knowledge-based view and cognitive and dynamic capabilities theory (Merendino et al., 2018). A comparative analysis uncovers that experienced, competent and professionally trained boards proactively facilitate innovation; conversely, family boards or those with informal hierarchy assist DT in a less organized way (Grove et al., 2021; Karayalcin, 2025; Yan & Yu, 2023; Zhao et al., 2025). Independent BODs show enhanced environmental performance and firm outcomes through innovation (Heubeck & Meckl, 2024). There is contrasting evidence regarding gender diversity on the board. From one standpoint, lower female participation has been correlated with higher DT level, while another documented that the significance of gender diversity has been independent of AI usage (Eroğlu & Karatepe Kaya, 2022; Figueroa-Domecq et al., 2020). From an analytical perspective, this evidence implies that the influence of DT on GC relies on the composition, structure, and capabilities of the board.

Within the IT governance and performance outcomes theme, the analyzed literature demonstrated ITG as a key pillar of good CG. ITG extends the framework, process, and expertise essential for consistent and credible service execution and operational oversight (Falchi de Magalhães et al., 2021; Tambo & Filtenborg, 2019). Literature highlights that even when organizations comply with legislative reporting requirements, insufficient internal control contributes to vulnerabilities, underscoring the critical need for standardized ITG frameworks to uphold data integrity and optimize efficiency (Chauke & Ngoepe, 2024). Additionally, analysis indicates that ITG mechanisms aligned with ITG principles, backed by top executives, elevate corporate outcomes and sustainability (Lowry et al., 2025). With the resource-based theoretical lens, research finds that DT capabilities advance ESG performance (Liu & Jung, 2024). Furthermore, AI and online social media have a positive impact on good CG (Capurro et al., 2023; Nasr et al., 2024; Shaban & Omoush, 2025).

Literature indicates that DT improves ESG practices through strengthening CG and fostering GI, notably among state-owned, large, and highly polluted enterprises (Xu et al., 2022). CG-supported innovation and digital economy elevate CSR activities, which further enhance economic value (Hu & Liu, 2023; Nazzaroi et al., 2022). Moreover, EMSC and EPSs boost GI (Ying & Jin, 2024). Nevertheless, despite the potential of AI to reinforce CG, organizations have to deal with growing digital risk. Digitalization presents cybersecurity threats, moral conundrums, and implementation difficulties (Grove et al., 2020; Kalkan, 2024). A critical cross-literature insight is that regulating technology-induced organizational risks through strong digital governance is vital for enduring sustainability benefits. Organizations must require a technology-enabled strategy balanced with human oversight and moral governance procedures.

Future Research Directions

Subsequent work could supplement the literature on DT and CG. There remains an avenue to examine board-level deployment of BDA across geographical and industrial contexts, and investigate how board members leverage these technologies (Karamatzanis et al., 2025). Another dimension requiring scholarly attention concerns whether the direct effect of the CEO’s digital technology orientation and the moderating effects of board characteristics also exist in smaller and younger firms, as well as in the business units of large publicly traded corporations. Additionally, identification of broader CG characteristics that might alter the focal association between the CEO’s digital technology orientation and stock market value would provide meaningful insights (Filatotchev et al., 2023).

A subsequent line of research could examine the influence of slack on output measures of innovation (e.g., patent count, new product development) and how this relationship is affected by board characteristics. Furthermore, the results are reproducible in more stakeholder-oriented CG systems, such as the German two-tiered board, as well as between more and less dynamic industries (Heubeck & Meckl, 2024). A further area for inquiry involves how board experience diversity shapes environmental innovation, notably via knowledge dissemination and multidisciplinary collaboration. Multi-context analysis and accounting for factors including firm size, industry, and competition could enhance understanding (Zhao et al., 2025). Subsequent research ought to investigate how family ties and socioeconomic wealth drive innovation within distinct cultural and institutional systems. Long-term assessment is required to observe top management succession influence on innovation (Karayalcin, 2025).

Another crucial issue is examining how DT affects internal control systems and the resulting economic effects (Wang et al., 2023). To ensure that corporate remuneration schemes are aligned with sustainability goals, prospective studies should also look at the implications of the digital age on equity incentive schemes and M&A models (Mu et al., 2023).

Future studies on DT, CG, and ER should fill the significant gaps by extending research contexts, including longitudinal analysis, and combined financial and non-financial measures. Existing literature has focused on large and listed firms; future work should concentrate on small and medium-sized enterprises (SMEs) that confront difficulties because of their low resources and unstructured decision-making. Examining the impact of external support, including government policies and financial assistance, on SMEs’ digital adoption could be insightful. Furthermore, there is a need for more research to understand the role of independent directors in decision-making, corporate performance, and board hierarchy (Yan & Yu, 2023). Additionally, cross-national comparative studies are required to assess the impact of organizational culture and economic disparities on the results of DT. Studies should also examine the time-lag effects of DT on enterprise performance and innovation (Liu & Jung, 2024).

Another key research area is the relationship between DT and ER in determining corporate sustainability and CSR. Prospective studies are recommended to investigate how ER can be applied to different nations and regulatory settings (Ying & Jin, 2024). The changing interplay between innovation, governance frameworks, and digitalization should also be the subject of future research. Extending the studies to non-listed enterprises and diverse industries will provide more generalizable conclusions (Capurro et al., 2023). Bridging these knowledge gaps will offer a foundational support for comprehending how CG mechanisms, ER, and DT collectively influence corporate outcomes.

Conclusion

This systematic literature review examined the interaction of DT and CG over the past decade (2014–2025). The analysis uncovered that DT has a significant impact on company strategies, governance frameworks, and decision-making, while a resilient governance framework fosters strategic and well-implemented DT. Technology-driven flexibility must be included in future CG mechanisms while maintaining governance’s resilience, ethics, and inclusivity. DT provides unmatched opportunities for CG efficacy, but how well enterprises handle its risks, obstacles, and ethical considerations will determine its success. Organizations may create sustainable governance frameworks that complement the changing digital economy by cultivating a digital responsible culture. This review demonstrates a thorough grasp of the existing literature on DT–CG interplay and its academic and practical significance.

Implications

There are significant ramifications for scholars, policymakers, and business executives. Employing a digital governance structure is essential for corporate leaders to preserve regulatory compliance and competitiveness. The BODs must ensure risk management and build digital capabilities.

Policymakers can outline a strategic framework and guidelines that drive transparency and board-level oversight, upholding public accountability. Also, there is a need to update governance legislation to ensure that emerging technologies adhere to legal, ethical, and ESG norms.

Researchers might further investigate effective AI-driven board decision-making, the role of technological ethics in governance, and the long-term effects of blockchain on transparency. Additionally, exploring the DT–CG relationship across multiple sectors and contexts, and using longitudinal and mixed-method designs, can generate more nuanced understandings.

Limitations

This study contributes to the understanding of DT in CG. Despite insightful findings, this study has certain limitations. It relies only on articles indexed in Scopus and Web of Science, which may introduce biases or coverage gaps. The study primarily concentrates on published articles and overlooks real-world situations and useful industry applications. Furthermore, digital technologies are developing so quickly that findings could become out of date. Inclusion of articles explicitly assessing DT–CG interaction potentially overlooked work concerning DT and CG exclusively but was relevant for comprehending the interaction. To improve the reliability of results, future research should include industry reports, expert interviews, and empirical case studies.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Almubarak, A. I., & Aljughaiman, A. A. (2024). Corporate governance and FinTech innovation: Evidence from Saudi Banks. Journal of Risk and Financial Management, 17(2), 48. https://doi.org/10.3390/jrfm17020048

Angulo, L. P., Slimane, F. B., & Alidou, D. (2014). The London stock exchange: Strategic corporate governance restructuring after demutualization. Journal of Applied Business Research, 30(1), 211. https://hal.science/hal-01128012

Capurro, R., Fiorentino, R., Galeotti, R. M., & Garzella, S. (2023). The impact of digitalization and sustainability on governance structures and corporate communication: A cross-industry and cross-country approach. Sustainability, 15(3), 2064. https://doi.org/10.3390/su15032064

Chauke, T. A., & Ngoepe, M. (2024). Integrating facets of information technology governance at a professional council in South Africa. Global Knowledge, Memory and Communication, 74(11), 101–120. https://doi.org/10.1108/gkmc-08-2023-0270

Cuervo, A. (2002). Corporate governance mechanisms: A plea for less code of good governance and more market control. Corporate Governance: An International Review, 10(2), 84–93. https://doi.org/10.1111/1467-8683.00272

Danilov, G. (2024). The impact of corporate governance on firm performance: Panel data evidence from S&P 500 information technology. Future Business Journal, 10(1), 86. https://doi.org/10.1186/s43093-024-00376-8

Ekaterina, K. (2025). Corporate governance in the context of business digital transformation. The American Journal of Management and Economics Innovations, 7(5), 90–98. https://doi.org/10.37547/tajmei/volume07issue05-11

Eroğlu, M., & Kaya, M. K. (2022). Impact of artificial intelligence on corporate board diversity policies and rregulations. European Business Organization Law Review, 23(3), 541–572. https://doi.org/10.1007/s40804-022-00251-5

Falchi de Magalhães, F. L., Gaspar, M. A., Luciano, E. M., & Napolitano, D. M. R. (2021). Information technology governance: Legitimation, theorization and field trends. Revista de Gestao, 28(1), 50–65. https://doi.org/10.1108/rege-01-2020-0001

Figueroa-Domecq, C., Palomo, J., Flecha-Barrio, M. D., & Segovia-Pérez, M. (2020). Technology double gender gap in tourism business leadership. Information Technology and Tourism, 22(1), 75–106. https://doi.org/10.1007/s40558-020-00168-0

Filatotchev, I., Lanzolla, G., & Syrigos, E. (2023). Impact of CEO’s digital technology orientation and board characteristics on firm value: A signaling perspective. Journal of Management, 51(2), 875–912. https://doi.org/10.1177/01492063231200819

Grove, H., Clouse, M., Schaffner, L., & Xu, T. (2020). Monitoring ai progress for corporate governance. Journal of Governance and Regulation, 9(1), 8–17. https://doi.org/10.22495/jgrv9i1art1

Grove, H., Clouse, M., & Xu, T. (2020). New risks related to emerging technologies and reputation for corporate governance. Journal of Governance and Regulation, 9(2), 64–74. https://doi.org/10.22495/jgrv9i2art4

Grove, H., Clouse, M., & Xu, T. (2021). Sustainable long-term value creation: New finance focus for boards of directors. Corporate Governance and Sustainability Review, 5(1), 22–30. https://doi.org/10.22495/cgsrv5i1p3

Guluma, T. F. (2021). The impact of corporate governance measures on firm performance: The influences of managerial overconfidence. Future Business Journal, 7(1), 50. https://doi.org/10.1186/s43093-021-00093-6

Heubeck, T., & Meckl, R. (2024). Does board composition matter for innovation? A longitudinal study of the organizational slack–innovation relationship in Nasdaq-100 companies. Journal of Management and Governance, 28(2), 597–624. https://doi.org/10.1007/s10997-023-09687-4

Hillman, A. J., Withers, M. C., & Collins, B. J. (2009). Resource dependence theory: A review. Journal of Management, 35(6), 1404–1427. https://doi.org/10.1177/0149206309343469

Hu, Y., & Liu, Q. (2023). Local digital economy and corporate social responsibility. Sustainability, 15(11), 8487. https://doi.org/10.3390/su15118487

Kalkan, G. (2024). The impact of artificial intelligence on corporate governance. Journal of Corporate Finance Research, 18(2), 17–25. https://doi.org/10.17323/j.jcfr.2073-0438.18.2.2024.17-25

Karamatzanis, G., Tilba, A., & Nikolopoulos, K. (2025). Corporate governance reporting, disclosures, monitoring, and decision-making: The role of big data analytics and technological tools. Corporate Governance: An International Review. https://doi.org/10.1111/corg.12646

Karayalcin, S. (2025). The effect of family vs. non-family CEOs on product innovation in Turkish family businesses. Administrative Sciences, 15(6), 200. https://doi.org/10.3390/admsci15060200

Levstek, A., Hovelja, T., & Pucihar, A. (2018). IT governance mechanisms and contingency factors: Towards an adaptive IT governance model. Organizacija, 51(4), 286–310. https://doi.org/10.2478/orga-2018-0024

Li, N., Wang, X., Wang, Z., & Luan, X. (2022). The impact of digital transformation on corporate total factor productivity. Frontiers in Psychology, 13, 1071986. https://doi.org/10.3389/fpsyg.2022.1071986

Li, X., Zhao, F., & Zhao, Z. (2024). Corporate digital transformation, internal control and total factor productivity. PloS One, 19(3), e0298633. https://doi.org/10.1371/journal.pone.0298633

Li, Z., Xie, B., Chen, X., & Fu, Q. (2024). Corporate digital transformation, governance shifts and executive pay-performance sensitivity. International Review of Financial Analysis, 92, 103060. https://doi.org/10.1016/j.irfa.2023.103060

Lin, Y., & Aman, A. B. (2025). The application of computer technology in corporate governance in the era of big data. WSEAS Transactions on Business and Economics, 22, 144–150. https://doi.org/10.37394/23207.2025.22.13

Liu, H., & Jung, J. S. (2024). Impact of digital transformation on ESG management and corporate performance: Focusing on the empirical comparison between Korea and China. Sustainability, 16(7), 2817. https://doi.org/10.3390/su16072817

Lowry, M. R., Lowry, P. B., Chatterjee, S., Moody, G. D., & Richardson, V. J. (2025). Achieving strategic alignment between business and information technology with information technology governance: The role of commitment to principles and Top leadership support. European Journal of Information Systems, 34(4), 610–635. https://doi.org/10.1080/0960085x.2024.2390998

Merendino, A., Dibb, S., Meadows, M., Quinn, L., Wilson, D., Simkin, L., & Canhoto, A. (2018). Big data, big decisions: The impact of big data on board-level decision-making. Journal of Business Research, 93, 67–78. https://doi.org/10.1016/j.jbusres.2018.08.029

Mu, Q., Zhang, W., & Hu, W. (2023). Enterprise transformation and innovation: A study of performance compensation from the perspective of information asymmetry. Sustainability, 15(17), 12826. https://doi.org/10.3390/su151712826

Napoli, F. (2023). Corporate digital responsibility: A board of directors may encourage the environmentally responsible use of digital technology and data: Empirical evidence from Italian publicly listed companies. Sustainability, 15(3), 2539. https://doi.org/10.3390/su15032539

Nasr, H. M. A., Emam, M. I. E., Ahmed, M. E. A., & Alshamrani, A. S. (2024). The role of artificial intelligence in supporting commercial companies governance. Journal of Ecohumanism, 3(4), 754–770. https://doi.org/10.62754/joe.v3i4.3587

Nazzaroi, C., Stanco, M., Uliano, A., Lerro, M., & Marotta, G. (2022). Collective smart innovations and corporate governance models in Italian wine cooperatives: The opportunities of the farm-to-fork strategy. International Food and Agribusiness Management Review, 25(5), 723–736. https://doi.org/10.22434/ifamr2021.0149

Nene, P. R. (2024). Can artificial intelligence replace assurance, governance and risk management professionals?. Risk Governance & Control: Financial Markets & Institutions, 14(2), 25–31. https://doi.org/10.22495/rgcv14i2p3

Oliveira, F., Kakabadse, N., & Khan, N. (2022). Board engagement with digital technologies: A resource dependence framework. Journal of Business Research, 139, 804–818. https://doi.org/10.1016/j.jbusres.2021.10.010

Ria, R. (2023). Determinant factors of corporate governance on company performance: Mediating role of capital structure. Sustainability, 15(3), 2309. https://doi.org/10.3390/su15032309

Shaban, O. S., & Omoush, A. (2025). AI-driven financial transparency and corporate governance: Enhancing accounting practices with evidence from Jordan. Sustainability, 17(9), 3818. https://doi.org/10.3390/su17093818

Shaohan, L. I. N., Kangqiao, X. U., Kongge, W. A. N. G., Huang, Y., Yating, Y. A. N. G., & Haojie, L. I. A. O. (2024). The intervention and impact of digital society on the governance of dual equity structure in enterprises. Revista de Cercetare Si Interventie Sociala, 86. 34–45. https://doi.org/10.33788/rcis.86.3

Tambo, T., & Filtenborg, J. (2019). Digital services governance: IT4ITTM for management of technology. Journal of Manufacturing Technology Management, 30(8), 1230–1249. https://doi.org/10.1108/jmtm-01-2018-0028

Thuy, N. T. T. (2025). Effect of accounting information system quality on decision-making success and non-financial performance: Does non-financial information quality matter? Cogent Business & Management, 12(1). https://doi.org/10.1080/23311975.2024.2447913

Varoglu, A., Gokten, S., & Ozdogan, B. (2021). Digital corporate governance: Inevitable transformation. Contributions to Finance and Accounting, Financial Ecosystem and Strategy in the Digital Era, 219–237. https://doi.org/10.1007/978-3-030-72624-9_10

Wang, C., Liu, X., & Li, Y. (2024). Exploring dynamic capability drivers of green innovation at different digital transformation stages: Evidence from listed companies in China. Sustainability, 16(13), 5666. https://doi.org/10.3390/su16135666

Wang, C., Wang, D., Deng, X., & Wang, S. (2023). Research on the impact of enterprise digital transformation on internal control. Sustainability, 16(2), 8392. https://doi.org/10.3390/su15108392

Xu, P., Chen, L., & Dai, H. (2022). Pathways to sustainable development: Corporate digital transformation and environmental performance in China. Sustainability, 15(1), 256. https://doi.org/10.3390/su15010256

Yan, A., & Yu, M. (2023). Board informal hierarchy and digital transformation: Evidence from Chinese manufacturing listed companies. Sage Open, 13(4). https://doi.org/10.1177/21582440231219086

Yang, X., Cao, D., Andrikopoulos, P., Yang, Z., & Bass, T. (2020). Online social networks, media supervision and investment efficiency: An empirical examination of Chinese listed firms. Technological Forecasting and Social Change, 154, 119969. https://doi.org/10.1016/j.techfore.2020.119969

Ying, Y., & Jin, S. (2024). Impact of environmental regulation on corporate green technological innovation: The moderating role of corporate governance and environmental information disclosure. Sustainability, 16(7), 3006. https://doi.org/10.3390/su16073006

Yu, J., Wang, J., & Moon, T. (2022). Influence of digital transformation capability on operational performance. Sustainability, 14(13), 7909. https://doi.org/10.3390/su14137909

Zhao, X., Wang, S., & Wu, X. (2025). Leveraging board experience diversity to enhance corporate green technological innovation. Sustainability, 17(8), 3351. https://doi.org/10.3390/su17083351

Zheng, J., Khurram, M. U., & Chen, L. (2022). Can green innovation affect ESG ratings and financial performance? Evidence from Chinese GEM listed companies. Sustainability, 14(14), 8677. https://doi.org/10.3390/su14148677